All Categories

Featured

Table of Contents

The are whole life insurance policy and universal life insurance policy. The money value is not included to the fatality benefit.

After ten years, the money worth has expanded to approximately $150,000. He obtains a tax-free funding of $50,000 to begin a company with his sibling. The policy car loan rate of interest is 6%. He pays off the loan over the following 5 years. Going this route, the interest he pays returns into his plan's cash money worth instead of a banks.

Infinite Banking Concept Wiki

The idea of Infinite Financial was produced by Nelson Nash in the 1980s. Nash was a finance professional and follower of the Austrian institution of business economics, which supports that the value of products aren't clearly the outcome of typical economic structures like supply and need. Rather, individuals value money and goods in a different way based upon their financial standing and requirements.

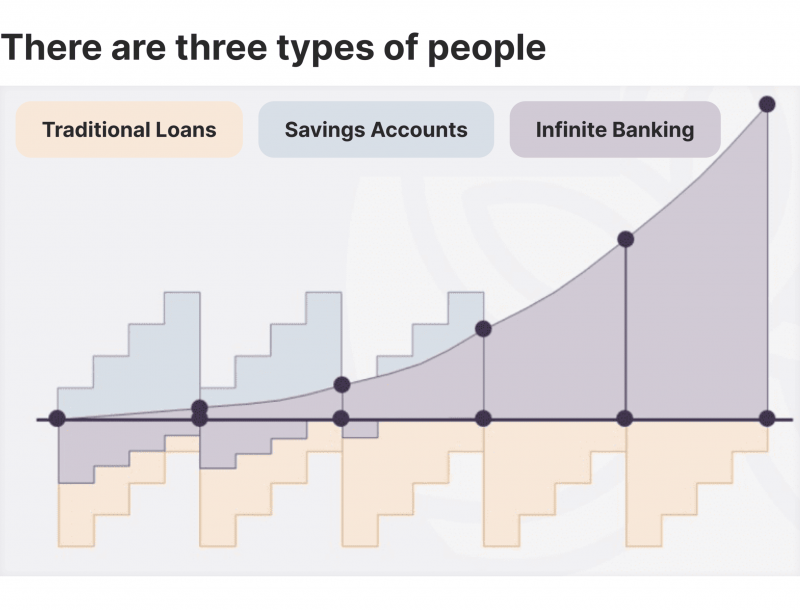

Among the mistakes of conventional banking, according to Nash, was high-interest prices on lendings. Way too many individuals, himself consisted of, entered into monetary difficulty as a result of reliance on banking establishments. Long as banks established the interest prices and lending terms, people didn't have control over their own riches. Becoming your very own banker, Nash determined, would put you in control over your financial future.

Infinite Banking needs you to own your financial future. For goal-oriented individuals, it can be the best monetary device ever. Here are the advantages of Infinite Financial: Probably the solitary most valuable aspect of Infinite Financial is that it boosts your money flow.

Dividend-paying whole life insurance policy is very low risk and supplies you, the insurance policy holder, a fantastic offer of control. The control that Infinite Financial uses can best be organized into two classifications: tax obligation advantages and possession protections.

Ibc Full Form In Banking

When you use whole life insurance coverage for Infinite Banking, you enter right into a private contract between you and your insurance coverage company. These protections might vary from state to state, they can include protection from possession searches and seizures, protection from judgements and defense from financial institutions.

Entire life insurance policy policies are non-correlated properties. This is why they work so well as the monetary structure of Infinite Banking. No matter of what takes place in the market (supply, genuine estate, or otherwise), your insurance coverage plan keeps its well worth.

Market-based financial investments grow riches much faster however are revealed to market variations, making them inherently high-risk. What if there were a 3rd pail that supplied safety but additionally modest, guaranteed returns? Whole life insurance is that 3rd container. Not just is the price of return on your whole life insurance policy policy ensured, your survivor benefit and costs are additionally guaranteed.

This framework lines up flawlessly with the concepts of the Continuous Wide Range Approach. Infinite Financial charms to those seeking higher economic control. Right here are its primary advantages: Liquidity and access: Plan fundings provide immediate accessibility to funds without the limitations of conventional bank lendings. Tax performance: The cash value expands tax-deferred, and plan loans are tax-free, making it a tax-efficient device for constructing riches.

Infinite Banking Real Estate

Asset security: In many states, the cash worth of life insurance policy is protected from lenders, including an additional layer of monetary security. While Infinite Banking has its benefits, it isn't a one-size-fits-all service, and it includes considerable disadvantages. Below's why it may not be the very best method: Infinite Banking typically needs complex policy structuring, which can perplex insurance policy holders.

Imagine never having to worry concerning small business loan or high rate of interest prices again. What if you could borrow money on your terms and develop wealth simultaneously? That's the power of unlimited financial life insurance policy. By leveraging the cash value of entire life insurance policy IUL plans, you can grow your wealth and obtain money without depending on standard financial institutions.

There's no collection lending term, and you have the flexibility to choose the settlement routine, which can be as leisurely as paying off the finance at the time of death. This versatility extends to the maintenance of the loans, where you can choose interest-only repayments, maintaining the loan balance level and workable.

Holding money in an IUL taken care of account being credited interest can frequently be far better than holding the cash on deposit at a bank.: You've always fantasized of opening your very own pastry shop. You can obtain from your IUL plan to cover the first costs of renting an area, purchasing tools, and working with team.

Infinite Banking Concept Book

Personal loans can be gotten from typical banks and credit score unions. Below are some bottom lines to consider. Credit report cards can provide an adaptable means to borrow money for extremely temporary durations. Nonetheless, borrowing cash on a credit history card is usually very expensive with interest rate of rate of interest (APR) typically reaching 20% to 30% or more a year.

The tax obligation therapy of plan lendings can vary dramatically depending upon your country of home and the specific regards to your IUL policy. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy loans are usually tax-free, providing a considerable advantage. Nonetheless, in various other territories, there might be tax ramifications to consider, such as possible taxes on the lending.

Term life insurance policy just supplies a survivor benefit, with no money worth buildup. This means there's no money worth to obtain versus. This short article is authored by Carlton Crabbe, Chief Exec Officer of Capital permanently, an expert in supplying indexed universal life insurance accounts. The info given in this short article is for educational and educational purposes only and must not be taken as monetary or financial investment guidance.

For lending police officers, the extensive guidelines enforced by the CFPB can be seen as troublesome and restrictive. Initially, finance officers commonly suggest that the CFPB's laws develop unneeded bureaucracy, leading to even more paperwork and slower funding processing. Rules like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) demands, while aimed at shielding customers, can result in hold-ups in shutting offers and increased operational costs.

{kind=link}

Latest Posts

Infinite Banking Concepts

'Be Your Own Bank' Mantra More Relevant Than Ever

How Infinite Banking Works